Education Loan or Saving for Your Child’s Education: Which Financial Choice Makes More Sense?

May 29, 2026

When it comes to financing your dreams or handling urgent financial needs, loans play a crucial role. Among the most popular options are personal loans and home loans. While both serve different purposes, many people often get confused about which one suits their needs better.

In this guide by KFINONE, we break down the essential differences between personal loans and home loans, along with key factors you should consider before making a decision.

Understanding Personal Loans and Home Loans

Before diving into the comparison, let’s understand what each loan type means.

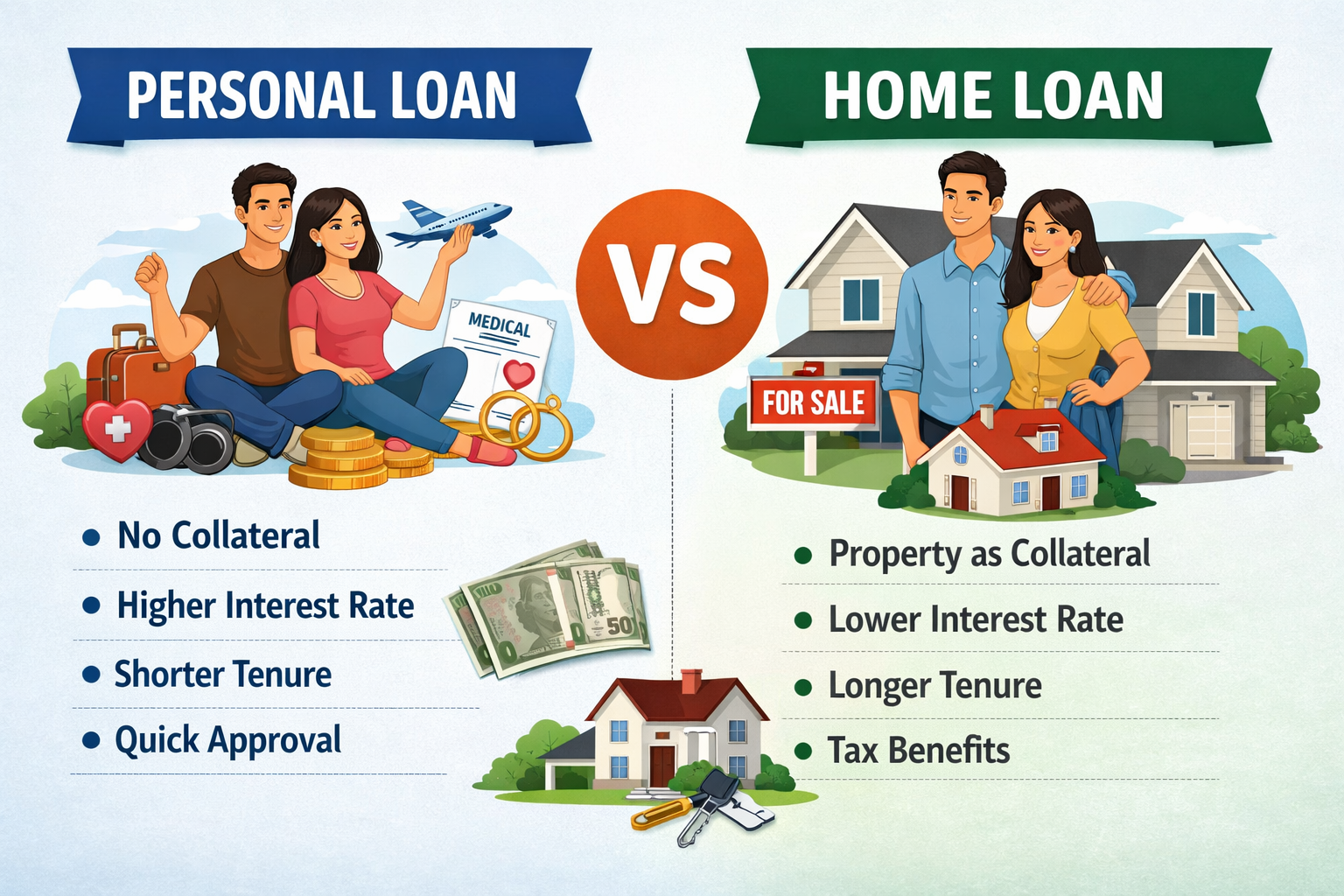

A personal loan is a type of financing that does not require any collateral and can be used for a wide range of needs, such as covering medical bills, planning a trip, managing wedding costs, or consolidating existing debts. Since it doesn’t require collateral, approval is usually faster, but interest rates tend to be higher.

A home loan is a type of secured financing offered to individuals for buying, building, or improving a residential property, where the property itself is used as collateral. The property itself acts as collateral, which allows lenders to offer lower interest rates and longer repayment tenures.

Personal Loan vs Home Loan: Major Differences Explained

1. Purpose of the Loan

Personal Loan: Flexible usage — you can use it for any personal financial need.

Home Loan: Strictly for property-related purposes like buying or building a house.

If you need funds for multiple purposes, a personal loan is ideal. For real estate investment, a home loan is the right choice.

2. Secured vs Unsecured

Personal Loan: Unsecured (no collateral required)

Home Loan: Secured (property is pledged as collateral)

Because home loans are secured, they come with lower risk for lenders and better terms for borrowers.

3. Interest Rates

Personal Loan: Higher interest rates (due to no collateral)

Home Loan: Lower interest rates (secured loan)

If affordability is your priority, home loans are more cost-effective in the long run.

4. Loan Amount

Personal Loan: Usually smaller amounts depending on income and credit score

Home Loan: Larger amounts based on property value

For big financial goals like buying a home, only a home loan can provide sufficient funding.

5. Repayment Tenure

Personal Loan: Shorter tenure (1–5 years)

Home Loan: Longer tenure (up to 30 years)

Home loans offer lower EMIs due to longer repayment periods, making them easier on your monthly budget.

6. Approval Process

Personal Loan: Quick approval and minimal documentation

Home Loan: Detailed verification and longer processing time

If you need urgent funds, personal loans are the faster option.

7. Tax Benefits

Personal Loan: No tax benefits (in most cases)

Home Loan: Tax deductions available on principal and interest

Home loans help you save money through tax benefits, making them financially smarter for long-term planning.

A personal loan is the right choice when:

For example, medical emergencies, travel expenses, or wedding costs are situations where a personal loan works best.

A home loan is ideal when:

Buying a home is a major life goal, and a home loan makes it achievable without putting financial pressure on you.

Key Factors to Consider Before Choosing

1. Your Financial

Goal Always start by identifying your purpose. If it's not related to property, a home loan won’t be applicable.

2. Repayment Capacity

Evaluate your monthly income and expenses. A long-term home loan requires financial discipline, while personal loans demand higher EMIs over a shorter period.

3. Interest Rate Comparison

Even a slight variation in interest rates can make a big difference in the overall amount you repay over the loan tenure. Always compare offers before choosing.

4. Credit Score

A good credit score helps you get better interest rates for both types of loans. Maintain a score above 750 for best deals.

5. Processing Time

If time is critical, personal loans are faster. Home loans involve property verification, which takes more time.

At KFINONE, we understand that every financial requirement is unique. That’s why we offer:

Whether you’re planning to buy your dream home or need funds for personal needs, KFINONE ensures a smooth and hassle-free loan experience.

Choosing between a personal loan and a home loan depends entirely on your financial goals, urgency, and repayment capacity.

Understanding these differences will help you make a smarter financial decision and avoid unnecessary burdens in the future.

Get the latest financial insights delivered to your inbox.